Show code

lasvegas <- read.csv("data/lasvegas.csv")Qualitative and Limited Dependent Variables

These problems accompany Qualitative and Limited Dependent Variables and its sub-pages on Binary Choice, Ordered Choice, and Multinomial Logit. Read those first for the theory behind these exercises.

Mortgage lenders are interested in determining borrower and loan characteristics that may lead to delinquency or foreclosure. In the data file

lasvegasare 1000 observations on mortgages for single family homes in Las Vegas, Nevada during 2008. The variable of interest is \(DELINQUENT\), an indicator variable = 1 if the borrower missed at least three payments (90+ days late), but 0 otherwise. Explanatory variables are \(LVR\) = the ratio of the loan amount to the value of the property; \(REF\) = 1 if the purpose of the loan was a “refinance” and = 0 if the loan was for a purchase; \(INSUR\) = 1 if the mortgage carries mortgage insurance, 0 otherwise; \(RATE\) = initial interest rate of the mortgage; \(AMOUNT\) = dollar value of mortgage (in \(\$100,000\)); \(CREDIT\) = credit score; \(TERM\) = number of years between disbursement of the loan and the date it is expected to be fully repaid, \(ARM\) = 1 if the mortgage has an adjustable rate, and = 0 if the mortgage has a fixed rate.

lasvegas <- read.csv("data/lasvegas.csv")Dependent variable:

Continuous regressors:

Binary regressors:

Estimate the linear probability model explaining \(DELINQUENT\) as a function of the remaining variables. Use White heteroskedasticity robust standard errors. Are the signs of the estimated coefficients reasonable?

Solution

vegas.lpm <- lm(DELINQUENT ~ ., data = lasvegas)

coeftest(vegas.lpm, vcov. = vcovHC(vegas.lpm, type = "HC1"))

t test of coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.6884913 0.2285064 3.013 0.002652 **

LVR 0.0016239 0.0006752 2.405 0.016360 *

REF -0.0593237 0.0240256 -2.469 0.013710 *

INSUR -0.4815849 0.0303694 -15.858 < 2e-16 ***

RATE 0.0343761 0.0098194 3.501 0.000484 ***

AMOUNT 0.0237680 0.0144509 1.645 0.100340

CREDIT -0.0004419 0.0002073 -2.132 0.033262 *

TERM -0.0126195 0.0035560 -3.549 0.000405 ***

ARM 0.1283239 0.0276932 4.634 4.07e-06 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1The signs on the estimated coefficients are reasonable. As the loan to home value ratio increases, the rate of delinquency increases. Refinanced loans are less likely to be delinquent, which is reasonable as banks would likely refinance individuals with a history of timely payments. The estimated coefficient indicates that mortgages that carry insurance (often for small down payments), are less likely to be delinquent. As interest rates increase, it is more likely that the loan becomes delinquent. As the credit score increases, it becomes less likely for the loan to be delinquent. As the term of the loan increases, it is less likely to become delinquent. Adjustable rate mortgages are more likely to become delinquent.

Use logit to estimate the model in (a). Are the signs and significance of the estimated coefficients the same as for the linear probability model?

Solution

vegas.logit <- glm(DELINQUENT ~ ., data = lasvegas, family = binomial(link = "logit"))

summary(vegas.logit)

Call:

glm(formula = DELINQUENT ~ ., family = binomial(link = "logit"),

data = lasvegas)

Coefficients:

Estimate Std. Error z value Pr(>|z|)

(Intercept) 1.66530 1.99216 0.84 0.40319

LVR 0.01352 0.00820 1.65 0.09916 .

REF -0.52506 0.23049 -2.28 0.02273 *

INSUR -3.12211 0.21691 -14.39 < 2e-16 ***

RATE 0.30866 0.08277 3.73 0.00019 ***

AMOUNT 0.21761 0.11377 1.91 0.05579 .

CREDIT -0.00356 0.00193 -1.84 0.06523 .

TERM -0.13304 0.03460 -3.85 0.00012 ***

ARM 1.40565 0.37136 3.79 0.00015 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

(Dispersion parameter for binomial family taken to be 1)

Null deviance: 998.03 on 999 degrees of freedom

Residual deviance: 666.29 on 991 degrees of freedom

AIC: 684.3

Number of Fisher Scoring iterations: 5The estimated coefficients all carry the same signs, however the coefficient on loan amount is now significant.

Compute the predicted value of \(DELINQUENT\) for the 500th and 1000th observations using both the linear probability model and the logit model. Interpret the values.

Solution

predict(vegas.lpm, lasvegas[c(500, 1000), ]) 500 1000

0.182783 0.578530 predict(vegas.logit, lasvegas[c(500, 1000), ], type = "response") 500 1000

0.133585 0.626553 For the 500th observation, the LPM predicts the individual had an \(18.3\%\) probability of delinquency, while the logit model predicted a \(13.4\%\) probability of delinquency. For the 1000th observation, the LPM predicts the individual had an \(57.9\%\) probability of delinquency, while the logit model predicted a \(62.7\%\) probability of delinquency.

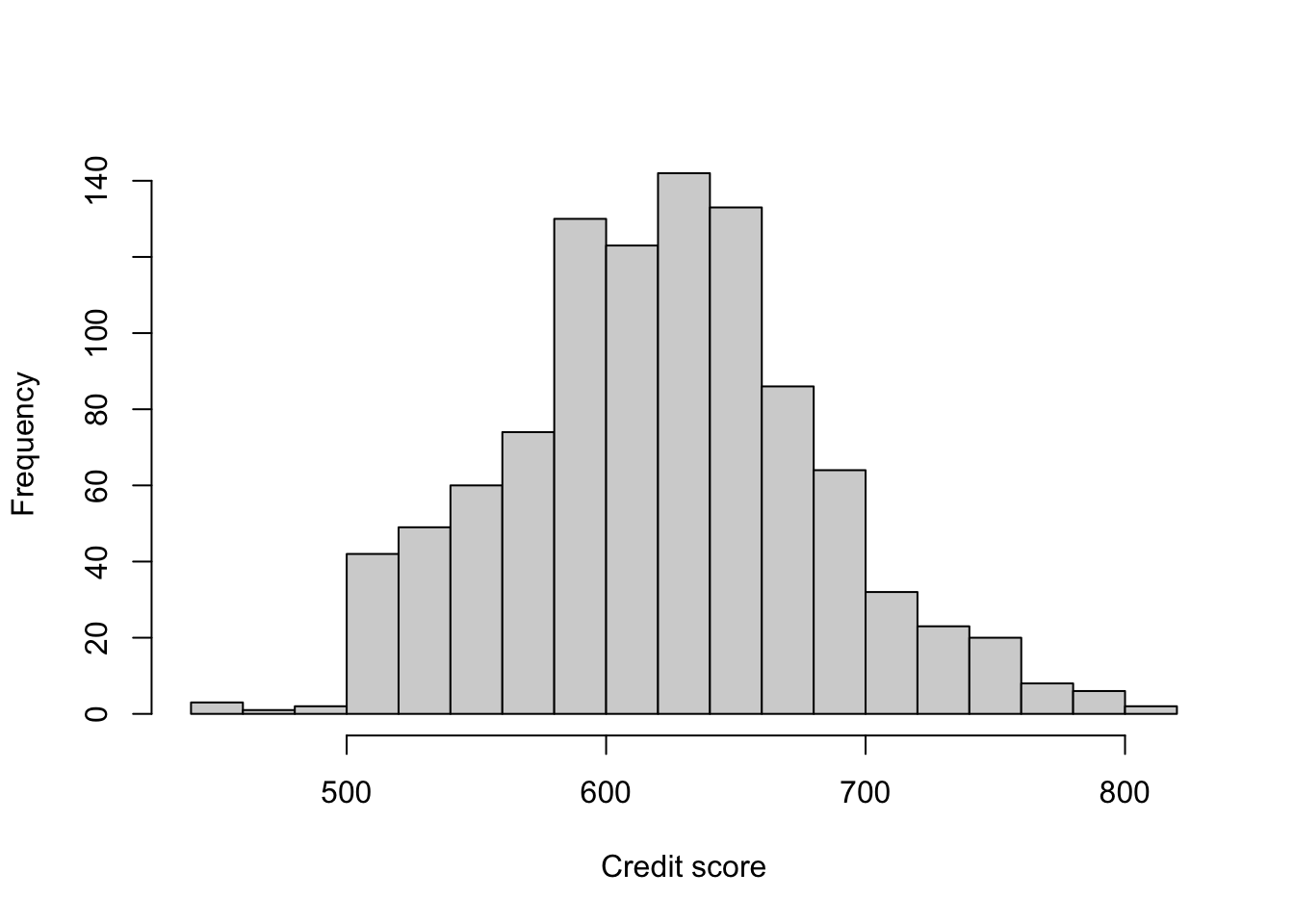

Construct a histogram of \(CREDIT\). Using both models, calculate the probability of delinquency for \(CREDIT\) = 500, 600, and 700 for a loan of \(\$250,000\). For the other variables, let the \(LVR\) be \(80\%\), the initial interest rate be \(8\%\), all indicator variables taking the value 0, and \(TERM = 30\). Discuss the similarities and differences among the predicted probabilities from the two models. Using both linear probability and logit models, compute the marginal effect of \(CREDIT\) on the probability of delinquency.

Solution

hist(lasvegas$CREDIT, main = "", xlab = "Credit score", breaks = 14)

## Predictions

characteristics <- data.frame(CREDIT = c(500, 600, 700),

AMOUNT = 2.5,

LVR = 80,

RATE = 8,

TERM = 30,

INSUR = 0,

REF = 0,

ARM = 0)

predict(vegas.lpm, characteristics) 1 2 3

0.553296 0.509106 0.464917 predict(vegas.logit, characteristics, type = "response") 1 2 3

0.496703 0.408631 0.326058 Given these loan characteristics, the logit model predicts lower rates of default across all credit scores. One interesting thing to note is the change in marginal effect. In the LPM, moving from a credit score of 500 to a credit score of 600 reduces default probability by the same amount as moving from a credit score of 600 to a credit score of 700. In both cases, the probability of default decreases by \(4.42\) percentage points. In comparison, the logit model has different marginal effects. Moving from 500 to 600 reduces the probability of default by \(8.81\) percentage points, while moving from 600 to 700 reduces the probability of default by \(8.26\) percentage points.

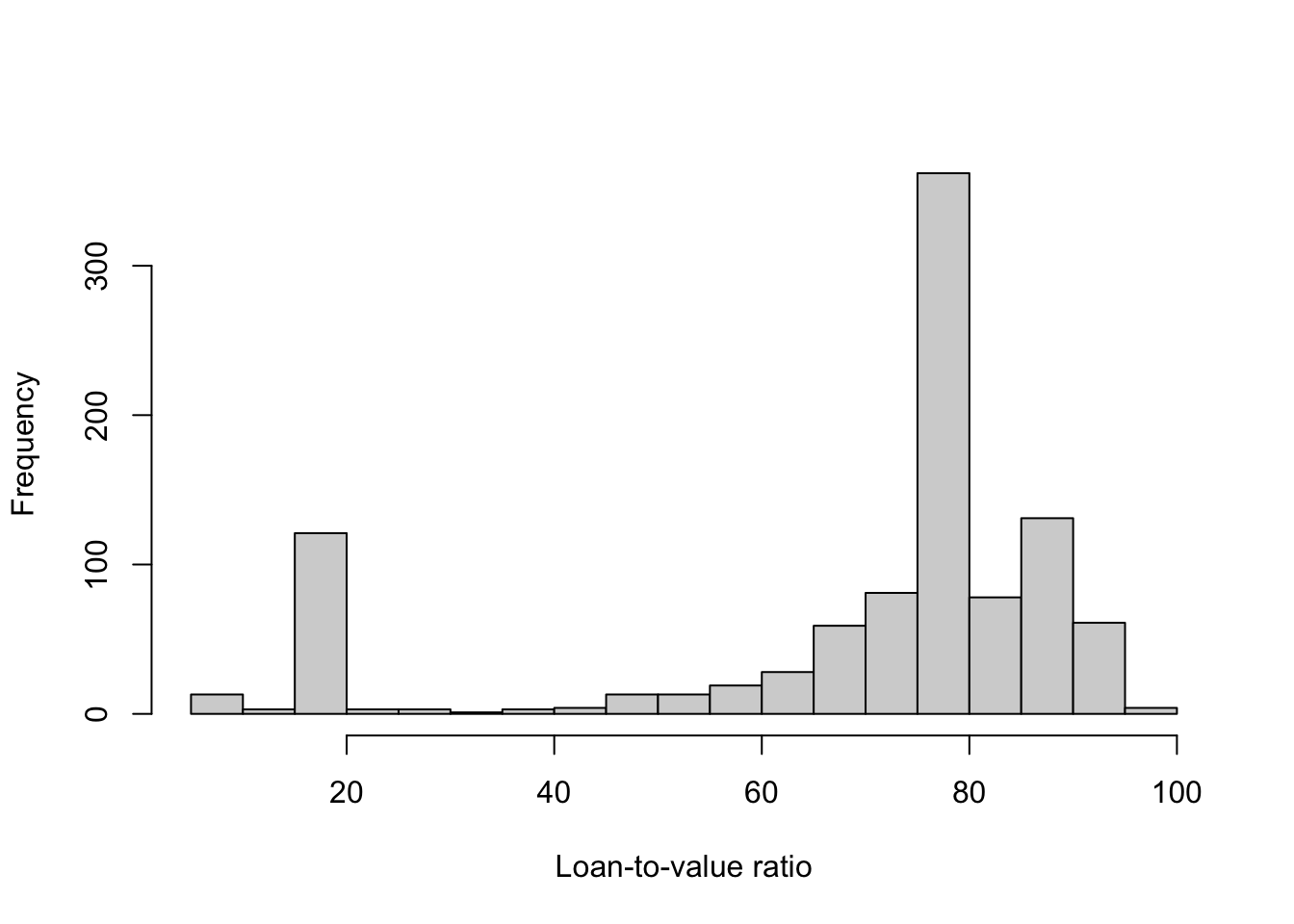

Construct a histogram of LVR. Using both the LPM and logit models, calculate the probability of delinquency for \(LVR = 20\) and \(LVR = 80\), with \(CREDIT = 600\) and other variables set as they are in (d). Compare and contrast the results.

Solution

hist(lasvegas$LVR, main = "", xlab = "Loan-to-value ratio", breaks = 14)

## Predictions

characteristics <- data.frame(CREDIT = 600,

AMOUNT = 2.5,

LVR = c(20, 80),

RATE = 8,

TERM = 30,

INSUR = 0,

REF = 0,

ARM = 0)

predict(vegas.lpm, characteristics) 1 2

0.411675 0.509106 predict(vegas.logit, characteristics, type = "response") 1 2

0.234909 0.408631 The logit model makes much lower predictions for delinquency probabilities than the linear model, and has a much larger marginal effect when moving from an \(LVR\) of 20% to an \(LVR\) of 80%.

Compare the percentage of correct predictions from the linear probability model and the logit model using a predicted probability of \(0.5\) as the threshold.

Solution

pred.lpm <- as.numeric(predict(vegas.lpm) > 0.5)

pred.logit <- as.numeric(predict(vegas.logit, type = "response") > 0.5)The linear probability model correctly predicts 858 delinquency outcomes, while the logit model correctly predicts 854.

As a loan officer, you wish to provide loans to customers who repay on schedule and are not delinquent. Suppose you have available to you the first 500 observations in the data on which to base your loan decisions on the second 500 applications (501–1,000). Is using the logit model with a threshold of \(0.5\) for the predicted probability the best decision rule for deciding on loan applications? If not, what is a better rule?

Solution

training.logit <- glm(DELINQUENT ~ ., data = lasvegas[1:500, ],

family = binomial(link = "logit"))

test.pred <- predict(training.logit, newdata = lasvegas[501:1000, ],

type = "response")

true.pred <- numeric(100)

for (i in 1:100) {

true.pred[i] <- sum(as.numeric(test.pred > i / 100) == lasvegas[501:1000, "DELINQUENT"])

}The threshold of \(0.5\) correctly predicts 440 applications in the test sample, while the optimal threshold of \(0.49\) accurately predicts 442 applications. However, this method does not account for the differences between a false positive vs. false negative. It is likely that loan officers would rather err on the side of caution and pick a cutoff that minimizes the likelihood of clearing a loan that turns delinquent, instead of a policy that incorrectly assumes someone will make delinquent payments.

How well do age, education, and other personal characteristics predict our assessment of our health status? Use the data file

rwm88to answer the following.

rwm88 <- read.csv("data/rwm88.csv")Tabulate the variable \(HSAT3\), which is a self-rating of health satisfaction, with \(1\) being the lowest and \(3\) being the highest. What percent of the sample assess their health status as \(HSAT3 = 1, 2,\) or \(3\)?

Solution

table(rwm88$hsat3)

1 2 3

1777 1792 914 Estimate an ordered probit model predicting \(HSAT3\) using \(AGE\), \(AGE^{2}\), \(EDUC2\) = years of education, and \(WORKING\) = 1 if employed. Which variables have coefficients that are statistically significant at the \(5\%\) level?

Solution

hsac.probit <- polr(factor(hsat3) ~ age + I(age^2) + educ2 + working,

data = rwm88, method = "probit")

summary(hsac.probit)Call:

polr(formula = factor(hsat3) ~ age + I(age^2) + educ2 + working,

data = rwm88, method = "probit")

Coefficients:

Value Std. Error t value

age -0.055709 0.0050842 -10.96

I(age^2) 0.000408 0.0000725 5.62

educ2 0.047848 0.0073468 6.51

working 0.091071 0.0382128 2.38

Intercepts:

Value Std. Error t value

1|2 -1.253 0.001 -1124.772

2|3 -0.119 0.023 -5.175

Residual Deviance: 9205.95

AIC: 9217.95 All the coefficients are statistically significant at the 5% level.

Estimate the marginal impact of age on the probabilities of health satisfactions \(HSAT3 = 1, 2,\) or \(3\) for someone age \(40\), with 16 years of education, and who is working.

Solution

Let \[\begin{align*} \hat{y}_{1} &= \hat\mu_{1} - \hat\beta_{1}AGE - \hat\beta_{2}AGE^{2} - \hat\beta_{3}EDUC2 - \hat\beta_{4}WORKING\\ \hat{y}_{2} &= \hat\mu_{2} - \hat\beta_{1}AGE - \hat\beta_{2}AGE^{2} - \hat\beta_{3}EDUC2 - \hat\beta_{4}WORKING \end{align*}\] The marginal effects are calculated with the following formula:

\[\begin{align*} \frac{\partial P(HSAT3 = 3|X)}{\partial AGE} &= \phi(\hat{y_{2}})\times(\beta_{1} + 2\beta_{2}AGE)\\ \frac{\partial P(HSAT3 = 2|X)}{\partial AGE} &= \left[\phi(\hat{y_{1}}) - \phi(\hat{y_{2}})\right]\times(\beta_{1} + 2\beta_{2}AGE)\\ \frac{\partial P(HSAT3 = 1|X)}{\partial AGE} &= - \phi(\hat{y_{1}})\times(\beta_{1} + 2\beta_{2}AGE)\\ \end{align*}\]

## Pull coefficients and X variables to plug into the predictions

coef <- as.numeric(hsac.probit$coefficients)

cutoffs <- as.numeric(hsac.probit$zeta)

characteristics <- c(40, 40^2, 16, 1)

## Calculate the latent values in the probit model

y1 <- cutoffs[1] - sum(coef * characteristics)

y2 <- cutoffs[2] - sum(coef * characteristics)

## Calculate the marginal effects

me3 <- dnorm(y2) * (coef[1] + 2 * coef[2] * characteristics[1])

me2 <- (dnorm(y1) - dnorm(y2)) * (coef[1] + 2 * coef[2] * characteristics[1])

me1 <- -dnorm(y1) * (coef[1] + 2 * coef[2] * characteristics[1])\[\begin{align*} \frac{\partial P(HSAT3 = 3|X)}{\partial AGE} &= -0.770\%\\ \frac{\partial P(HSAT3 = 2|X)}{\partial AGE} &= -0.030\%\\ \frac{\partial P(HSAT3 = 1|X)}{\partial AGE} &= 0.800\%\\ \end{align*}\]

(Note that the marginal effects add up to zero!)

Estimate the marginal impact of age on the probabilities of health satisfaction \(HSAT3 = 1, 2,\) or \(3\) for someone age \(70\), with 16 years of education, and who is working.

Solution

## Pull coefficients and X variables to plug into the predictions

coef <- as.numeric(hsac.probit$coefficients)

cutoffs <- as.numeric(hsac.probit$zeta)

characteristics <- c(70, 70^2, 16, 1)

## Calculate the latent values in the probit model

y1 <- cutoffs[1] - sum(coef * characteristics)

y2 <- cutoffs[2] - sum(coef * characteristics)

## Calculate the marginal effects

me3 <- dnorm(y2) * (coef[1] + 2 * coef[2] * characteristics[1])

me2 <- (dnorm(y1) - dnorm(y2)) * (coef[1] + 2 * coef[2] * characteristics[1])

me1 <- -dnorm(y1) * (coef[1] + 2 * coef[2] * characteristics[1])\[\begin{align*} \frac{\partial P(HSAT3 = 3|X)}{\partial AGE} &= 0.035\%\\ \frac{\partial P(HSAT3 = 2|X)}{\partial AGE} &= 0.018\%\\ \frac{\partial P(HSAT3 = 1|X)}{\partial AGE} &= -0.052\%\\ \end{align*}\]

Estimate the marginal impact of \(WORKING\) on the probabilities of health satisfaction \(HSAT3 = 1, 2,\) or \(3\) for someone age \(40\), with 16 years of education.

Solution

In this example, we just take differences in probabilities to compute the marginal effects, e.g.

\[ \frac{\Delta P(HSAT3 = 1|X)}{\Delta WORKING} = P(HSAT3 = 1|X, WORKING = 1) - P(HSAT3 = 1|X, WORKING = 0) \]

## Pull coefficients and X variables to plug into the predictions

coef <- as.numeric(hsac.probit$coefficients)

cutoffs <- as.numeric(hsac.probit$zeta)

characteristics0 <- c(40, 40^2, 16, 0)

characteristics1 <- c(40, 40^2, 16, 1)

## Calculate the latent values in the probit model

me1 <- pnorm(cutoffs[1] - sum(coef * characteristics1)) -

pnorm(cutoffs[1] - sum(coef * characteristics0))

me3 <- pnorm(cutoffs[2] - sum(coef * characteristics0)) -

pnorm(cutoffs[2] - sum(coef * characteristics1))

me2 <- -(me1 + me3)\[\begin{align*} \frac{\Delta P(HSAT3 = 3|X)}{\Delta WORKING} &= 2.948\%\\ \frac{\Delta P(HSAT3 = 2|X)}{\Delta WORKING} &= 0.277\%\\ \frac{\Delta P(HSAT3 = 1|X)}{\Delta WORKING} &= -0.3225\% \end{align*}\]

In this exercise, we use multinomial logit to describe factors leading an individual to fall into one of three categories. Use data file

rwm88for this exercise.

Create a variable called \(INSURED\) = 1, if a person does not have public insurance or add-on insurance (\(PUBLIC\) = 0 and \(ADDON\) = 0). Let \(INSURED\) = 2 if (\(PUBLIC\) = 1 and \(ADDON\) = 0). Let \(INSURED\) = 3 if (\(PUBLIC\) = 1 and \(ADDON\) = 1). Tabulate the number of individuals falling into each category. How many individuals are accounted for?

Solution

rwm88 <- read.csv("data/rwm88.csv")

rwm88$insured <- NA

rwm88$insured[rwm88$public == 0 & rwm88$addon == 0] <- 1

rwm88$insured[rwm88$public == 1 & rwm88$addon == 0] <- 2

rwm88$insured[rwm88$public == 1 & rwm88$addon == 1] <- 3

addmargins(table(rwm88$insured))

1 2 3 Sum

572 3778 133 4483 Estimate a multinomial logit model with outcome variable \(INSURED\) and explanatory variables \(AGE\), \(FEMALE\), \(WORKING\), and \(HHNINC2\). Use \(INSURED\) = 1 as the base category. What information is provided by the signs and significance of the estimated coefficients?

Solution

multi.mod <- multinom(insured ~ age + female + working + hhninc2, data = rwm88)# weights: 18 (10 variable)

initial value 4925.078890

iter 10 value 2684.428978

iter 20 value 2180.448628

iter 30 value 2179.310098

final value 2179.269281

convergedmulti.modCall:

multinom(formula = insured ~ age + female + working + hhninc2,

data = rwm88)

Coefficients:

(Intercept) age female working hhninc2

2 2.72766 0.0090408 0.32103 -0.213368 -0.0003223915

3 -1.99340 0.0178451 0.43059 -0.377003 -0.0000403559

Residual Deviance: 4358.54

AIC: 4378.54 Positive coefficients indicate an increased probability of the alternative to the base alternative. Thus for \(INSURED\) = 2, \(AGE\) and \(FEMALE\) increase the probability of public insurance rather than no insurance, while higher income reduces the probability of having public insurance relative to no insurance. For \(INSURED\) = 3, \(AGE\) and \(FEMALE\) increase the probability of having public insurance and add-on insurance rather than no insurance.

Obtain the predicted probabilities of falling into each category for each person in the sample, calling them \(P1\), \(P2\), and \(P3\). Find the sample averages of \(P1\), \(P2\), and \(P3\) and compare these to the percentages of the sample for whom \(INSURED\) = 1, 2, and 3, respectively.

Solution

# Sample average of probability of being 1, 2, 3

colMeans(predict(multi.mod, type = "prob")) 1 2 3

0.1275932 0.8427392 0.0296676 # Actual observations of 1, 2, 3

prop.table(table(rwm88$insured))

1 2 3

0.1275931 0.8427392 0.0296676 The average probabilities and shares match exactly. This is a property of multinomial logit.

Obtain the predicted probabilities of falling into each category for a person who is 50 years old, female, working and with a household income, \(HHNINC2\) = 2400.

Solution

values <- data.frame(age = 50, female = 1, working = 1, hhninc2 = 2400)

predict(multi.mod, values, type = "prob") 1 2 3

0.0731639 0.9035399 0.0232963 Repeat the calculations in (d) for \(HHNINC2\) = 4200.

Solution

values <- data.frame(age = 50, female = 1, working = 1, hhninc2 = 4200)

predict(multi.mod, values, type = "prob") 1 2 3

0.1218252 0.8421020 0.0360727 Calculate the 25th and 75th percentiles of \(HHNINC2\). Comment on the changes in probabilities computed in parts (d) and (e).

Solution

quantile(rwm88$hhninc2, c(0.25, 0.75)) 25% 75%

2400 4200 The 25th percentile value is 2400, and 75th percentile value is 4200. Thus the changes in the probabilities in parts (d) and (e) reflect the difference of 50 percentile points in income. For both non-default options, the choice probability decreases in household income. However, the effect on the second option is much more pronounced. This means that, on average, individuals will move from groups 2 and 3 to the default option. However, some individuals in group 2 will move to group 3 before they move to the default option.

Thank you to Coleman Cornell for generously sharing his materials with me.